South Park Condo Market Snapshot — April 2026 By Michael Robleto

The South Park condo market remains slow, though we are beginning to see some modest improvements in transaction activity and pricing. This monthly column tracks key metrics within the South Park BID boundary to provide a consistent view of supply, pricing, and buyer activity in the neighborhood.

All data is sourced from the MLS and includes only condominium buildings located within the South Park Business Improvement District.

About the Author

This report is compiled by Michael Robleto, a South Park resident and real estate broker with Compass who specializes in Downtown Los Angeles condominium buildings and Eastside residential markets including Pasadena, Los Feliz, and Highland Park. Michael has lived in South Park since 2009 and closely tracks neighborhood sales data, pricing trends, and building-specific market activity.

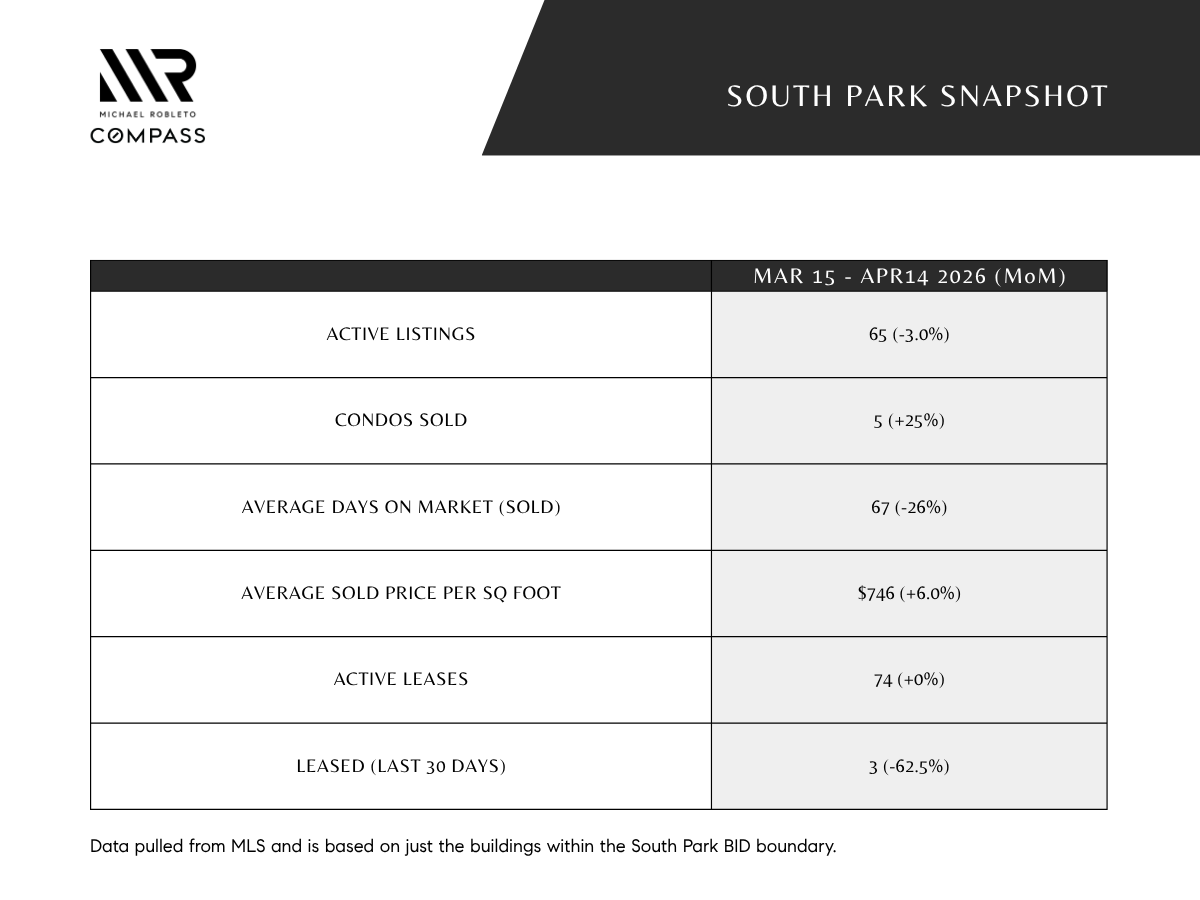

Active inventory remained relatively stable, decreasing slightly from 67 to 65 units. Sales activity increased modestly with five closings during the period, up from four in the prior snapshot.

Average days on market dropped significantly from 91 days to 67 days, reinforcing that well-positioned units—those with views, updated interiors, and realistic pricing—are continuing to find buyers.

Pricing Trends

The average sold price per square foot (PPSF) increased to $746, up from $704 in the previous report and $685 in January.

One sale at Ten50 skewed the average higher this month, but even when removing that transaction, pricing still came in roughly $20 per square foot above the prior period. That is a meaningful signal in a market that has otherwise been trending flat.

It is also worth noting that PPSF typically softens during the winter months. Any upward movement as we move into spring is generally a positive sign, even if modest.

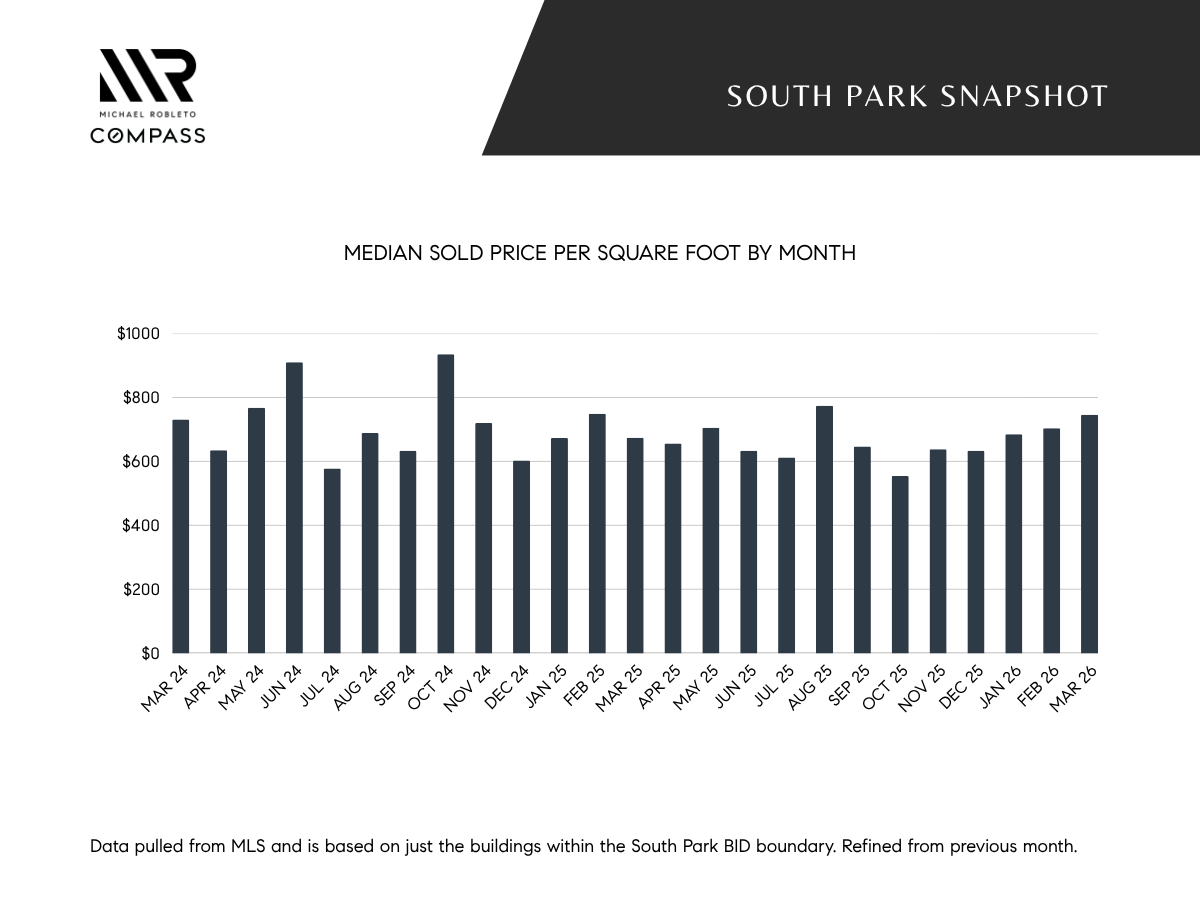

The chart below tracks the median sold price per square foot by month since early 2024.

While monthly data can be volatile due to low transaction volume, pricing overall continues to hold within a relatively stable range.

Market Interpretation

The current snapshot points to a market that is still slow, but not without selective strength.

Sales volume increased, though only by one additional unit, which highlights the continued lack of depth in the buyer pool. Typically, early spring brings increased condo demand driven in part by what agents refer to as the “USC effect,” where parents purchase units for students entering their second or third year. Similar to last year, we are not seeing that demand materialize in a meaningful way.

At the same time, the sharp reduction in days on market suggests that buyers are still active when the product is compelling. Units that are priced correctly and present well are moving. Everything else is sitting.

Leasing activity weakened significantly this period, with only three units leased in the past 30 days. This is a notable drop and may reflect increased competition as well as seasonal timing. Leasing demand typically strengthens heading into the summer months, so this will be an important metric to watch in the next report.

Broader Context

Despite some improvement in pricing and days on market, the broader market remains challenging.

Many sellers are continuing to transact at or below their original purchase price, reinforcing the reality that buyers currently control the market. LINK: https://www.bungalowagent.com/blog/2026/4/1/most-dtla-condo-sellers-are-losing-money-buyers-now-control-the-market

A significant factor behind the slowdown is perception around livability. Downtown Los Angeles is not currently viewed by many buyers as a primary or long-term housing choice, particularly when compared to other Los Angeles neighborhoods. This is in contrast to the experience of many current residents, who would strongly disagree with that characterization.

Looking Ahead

The key indicators to watch heading into late spring and early summer will be:

Whether sales volume continues to increase

Whether leasing demand rebounds

Whether pricing continues to firm modestly above winter levels

The market is showing early signs of improvement in select areas, but overall conditions remain slow and highly dependent on pricing and product quality.

Next month’s report will provide further clarity as we move deeper into the traditional spring selling season.